In the world of real estate, especially in the commercial sector, some terms and acronyms may seem unfamiliar to those new to the field. One such term is TMI, which stands for Taxes, Maintenance, and Insurance.

This term is often used in the context of commercial leasing, where the tenant is typically responsible for these costs in addition to their base rent.

The concept of TMI is crucial in understanding the financial obligations involved in a commercial lease agreement.

Elements of TMI

TMI stands for Taxes, Maintenance, and Insurance. These are the three main components of the total monthly investment (TMI) that a property owner or tenant has to pay for a real estate property. TMI is an important concept in real estate finance, as it helps measure a property’s profitability and affordability.

Taxes

Property taxes, a crucial component of TMI, involve monetary payments to local authorities. These payments are calculated based on the assessed value of the property and the current tax rates. They represent taxes imposed on the owners of real estate assets, including land, buildings, and other structures.

The property tax one must pay is typically determined by the assessed value of their property.

British Columbia

Ontario

New Brunswick

Quebec

Newfoundland & Labrador

While Vancouver is known for having the lowest property tax rate in Canada, it’s also renowned for its high-priced homes, with average prices exceeding $1 million. Typically, cities like Vancouver and Toronto, with high property values, have lower property taxes. Conversely, cities with lower property values tend to have higher tax rates.

Maintenance

Maintenance costs, a vital part of TMI, cover the expenses needed to keep a property in its best condition. These costs, ranging from regular repairs to significant maintenance, play a substantial role in TMI.

The “1% rule” suggests that homeowners should set aside 1% of their property’s purchase price each year for maintenance costs. For example, if you purchased a home for $500,000, you would allocate $5,000 per year for maintenance. However, some experts view this allocation as conservative and recommend reserving as much as 3% to 5% instead. Therefore, maintaining a $500,000 home in good condition could necessitate an annual budget of $15,000 to $25,000.

| Did you know? Between two similar buildings, the one with more units may have lower fees. However, more units can result in greater wear and tear, potentially costing more to maintain over time. |

Another method is the “square footage rule,” where homeowners reserve $1 per square foot of their property’s size for maintenance and repairs. While this strategy recognizes that larger homes may require more maintenance, it doesn’t consider various factors affecting costs.

For example, newer homes won’t need immediate appliance replacements regardless of their size. Additionally, costs are influenced by location, including labour costs, a significant factor for non-DIY repairs.

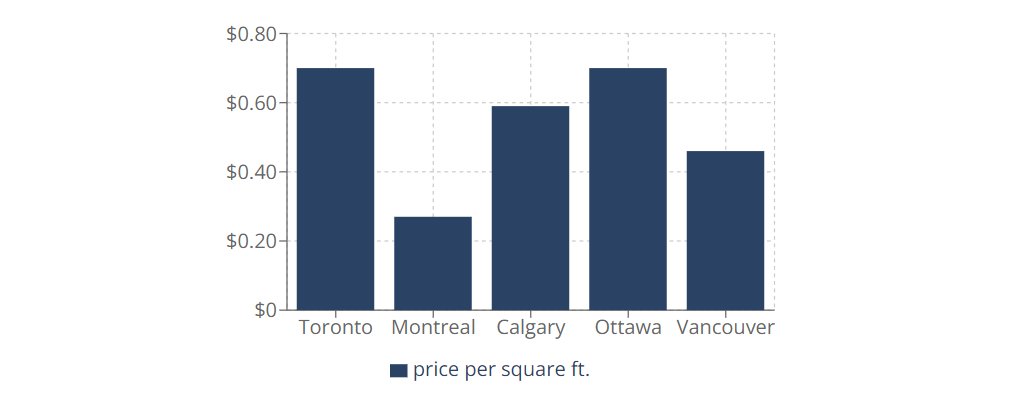

If you reside in a Toronto condo, monthly fees can vary significantly and often rise as the building gets older. They range from approximately $0.60 to $0.75 per square foot, so for a 600-square-foot unit, you might pay between $360 and $450 per month. Larger units will have higher fees, with 1,000 square feet costing $600 to $750 or more monthly.

Did you know?

Insurance

Insurance in real estate serves as a safety shield within TMI, providing a safeguard against unexpected incidents that could affect the property’s value. The expenses related to insurance act as a protective layer for both landlords and tenants.

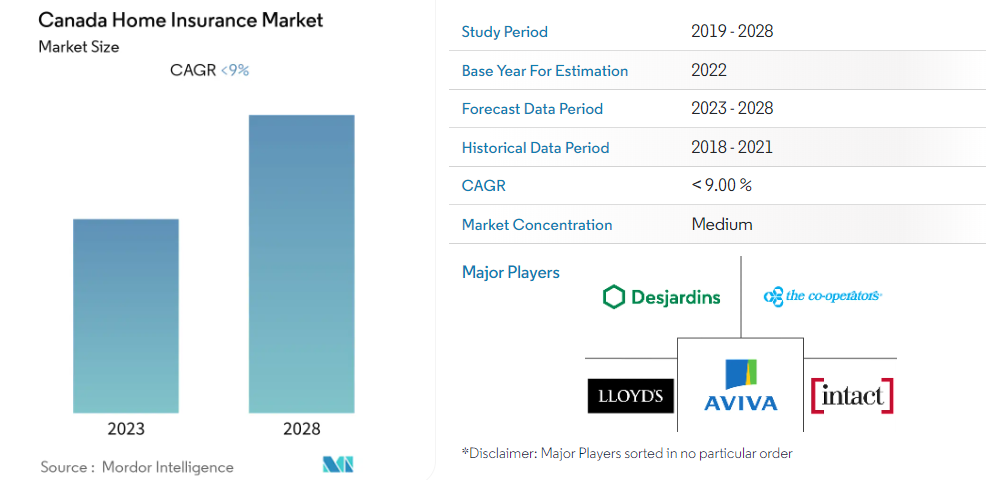

In 2023, the average annual cost of home insurance in Canada is around $1,100. However, due to the diverse range of policyholders, there are significant variations in home insurance costs, influenced by several factors. A key factor is your geographical location, with different provinces having different average rates.

For example, Ontario and British Columbia typically have significantly higher rates compared to the Maritime provinces. Furthermore, the specific policy you choose and the details of your coverage also affect home insurance rates.

| Did you know? Ontario has a property tax deferral program for seniors, allowing them to defer part or all of their property taxes until they sell their home. |

How to Calculate TMI?

Calculating TMI is like putting together the pieces of a puzzle. This total allows both tenants and landlords to assess the overall financial obligation tied to the property.

Consider an example for 3,000 square feet of office space: $12.00 base rent + $8.00 TMI.

The calculation would be as follows:

$12.00 (Net Rent)+$8.00 (TMI)=$20.00 (Gross Rent per sq. ft.)$12.00 (Net Rent)+$8.00 (TMI)=$20.00 (Gross Rent per sq.ft.)

Then, multiply the Gross Rent by the total square footage:

$20.00×3,000 sq.ft.=$60,000.00 annually$20.00×3,000 sq.ft.=$60,000.00 annually

This translates to monthly payments of:

$60,000.00÷12=$5,000.00 per month$60,000.00÷12=$5,000.00 per month

Please note that a 13% HST would be added to this amount.

The Importance of TMI in Real Estate

Total Monthly Investment (TMI) is a fundamental concept in real estate that encapsulates the various costs associated with owning or leasing a property. These costs include property taxes, maintenance charges, and insurance premiums. TMI allows sellers to strategically price properties and assists buyers in evaluating affordability.

The dynamic nature of TMI, influenced by fluctuating factors such as property tax assessments, insurance rates, and maintenance costs, highlights the importance of constant vigilance. TMI also plays a crucial role in commercial lease negotiations, offering strategies for both buyers and sellers.

Navigating TMI negotiations can be complex due to variable costs, the balance between property maintenance and cost reduction, and evolving real estate market trends. However, with well-defined lease terms, transparency, and provisions for managing TMI fluctuations, both landlords and tenants can successfully navigate TMI negotiations.

The Impact of TMI on Property Pricing

The combination of property taxes, maintenance expenses, and insurance costs, collectively known as TMI, provides a comprehensive picture of the financial obligations associated with a property. This allows sellers to competitively price their properties, taking into account both the tangible assets and the intangible responsibilities that come with the property.

Furthermore, buyers equipped with TMI information can make more precise evaluations of what they can afford, facilitating a smoother and more efficient negotiation process.

Strategies for Negotiating TMI in a Lease

Negotiating TMI is a critical aspect of entering into a commercial lease agreement. Tenants looking for favourable terms can consider the following strategies:

- Clear Lease Terms: It’s essential to ensure that the lease terms clearly define the responsibilities of both parties regarding TMI to prevent future disagreements.

- Transparency: Asking for transparency in the breakdown of TMI components—property taxes, maintenance, and insurance—can set the stage for fair negotiations.

- Contingencies: Incorporating provisions for managing TMI fluctuations due to unexpected circumstances can alleviate potential financial stress.

For landlords, showing flexibility and a willingness to negotiate can foster goodwill and strengthen relationships with tenants.

Overcoming Challenges in TMI Negotiations

Negotiating TMI can be a complex process, fraught with challenges. Both parties must navigate intricate dynamics that span various aspects, including:

- Variable Costs: The unpredictability of property tax assessments, maintenance requirements, and insurance rates adds an element of uncertainty to negotiations.

- Balancing Act: Achieving a balance between maintaining the property’s condition and minimizing costs is a delicate task that influences TMI calculations.

- Market Trends: Fluctuating real estate market trends can affect property values, which indirectly impact TMI components like property taxes.

Understanding these challenges can help both parties negotiate more effectively and reach mutually beneficial agreements.

FAQ

What does TMI mean in Real Estate?

In real estate, TMI refers to taxes, maintenance, and insurance. It represents the additional expenses that tenants are responsible for in a commercial lease, apart from the base rent.

What is included in TMI Ontario?

In Ontario, TMI encompasses property taxes, maintenance fees, and insurance premiums. It may also include utilities, property management fees, and common area maintenance costs.

How is TMI calculated in a commercial lease?

TMI is determined by summing up the annual costs of property taxes, insurance, and maintenance, dividing this total by the building’s total square footage, and then multiplying by the tenant’s square footage.

Can TMI fluctuate over time?

Yes, TMI can vary due to changes in property taxes, insurance premiums, and maintenance costs, which may differ annually.

How to insure business against rising TMI costs?

To safeguard against increasing TMI costs, try to negotiate a lease with a fixed TMI rate, ensuring these costs remain constant throughout the lease term.

What does TMI mean in Construction?

In construction, TMI stands for Trade, Material, and Equipment. It refers to the costs associated with the materials, equipment, and labour required for a construction project.

What are the hidden costs of triple net leases?

The hidden costs of triple net leases may include substantial maintenance expenses, fluctuating property taxes, and insurance premiums that tenants are responsible for in addition to the base rent.

TMI in Real Estate – Final Words

Grasping the complex components of TMI in real estate is crucial for making informed decisions in property transactions. These elements—Taxes, Maintenance, and Insurance—constitute the additional costs that significantly influence the total expense of occupying or owning a property.

A thorough understanding of these factors allows tenants and property owners to effectively budget, plan, and negotiate lease terms or property purchases. Furthermore, it aids in better financial management by forecasting and accounting for ongoing expenses, ensuring a more precise evaluation of the overall investment.

Whether considering commercial or residential properties, acknowledging the implications of TMI enables prudent financial planning, risk reduction, and informed choices in the dynamic realm of real estate. This empowers individuals and businesses to navigate the market with assurance and clarity.

Be First to Comment