Inheriting property following the passing of a loved one can evoke mixed emotions. While it can offer financial advantages, complexities regarding taxes, particularly the Land Transfer Tax (LTT) in Ontario, often accompany this process. Let’s explore the nuances of LTT in Ontario as it relates to inherited real estate.

Understanding Land Transfer Tax (LTT) Basics

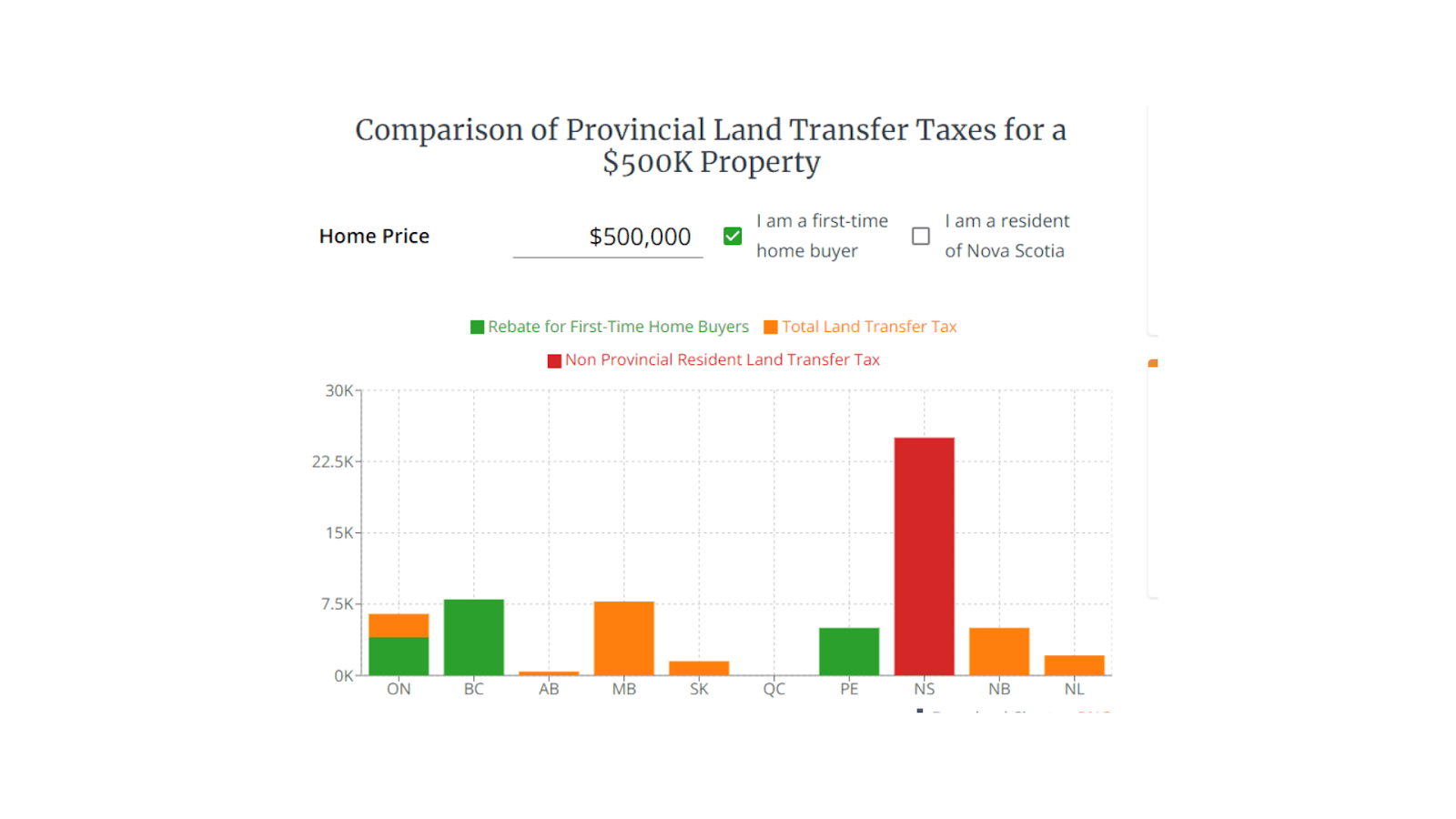

The Land Transfer Tax is a provincial levy imposed on real estate exchanges in Ontario. This tax is charged when property is sold, bought, or transferred, contributing to public funds and municipal resources. It’s essential to note that LTT rates and rules may differ across provinces.

LTT and Inherited Property: The General Rule

Normally, when property changes hands, LTT applies. However, in Ontario, inherited properties generally receive an exemption from LTT following the owner’s death. This exemption also extends to property transferred to a spouse due to a separation agreement or a court order.

Factors Influencing LTT on Inherited Property

Despite the exemption for inherited properties, several scenarios might still trigger LTT:

- Will Stipulations

If the deceased instructs the executor to sell the property and distribute the proceeds, LTT may apply since the property technically changes hands.

- Multiple Beneficiaries

In cases where a property is bequeathed to multiple beneficiaries and one heir buys out others, LTT might be applicable based on the value of the transferred property share.

- Beneficiary Residing Outside Ontario

While an initial inheritance in Ontario avoids LTT for beneficiaries residing elsewhere, subsequent property sales by non-Ontario residents attract LTT.

- Estate Planning and LTT’s Role

Efficient estate planning is crucial for managing inherited property complexities. It aids in minimizing tax liabilities and ensuring smooth property ownership transitions. Seeking legal advice on estate planning, particularly regarding LTT implications, is advisable.

Who Pays LTT in Ontario?

LTT is paid when acquiring land in Ontario, except in specific circumstances, such as transferring land to a spouse, family corporation, farming relatives, or a charity. First-time homebuyers might also qualify for LTT rebates.

LTT Calculation in Ontario

In Ontario, LTT is a percentage of the land acquisition amount, considering any remaining mortgage or debt. The rates follow a tiered structure:

- 0.5% for up to $55,000

- 1.0% from $55,000 to $250,000

- 1.5% from $250,000 to $400,000

- 2.0% from $400,000

- 5% on values over $2,000,000 for single-family residences

Exemptions to LTT in Ontario

Various exemptions and rebates can reduce LTT burdens, including:

- First-time Homebuyer Rebate

- Farm Property Rebate

- Primary Residence Exemption

LTT in Estate Transfers

In estate transfers, LTT applicability differs based on the presence or absence of a will and the number of beneficiaries involved.

- With a Will: Transfer to a sole beneficiary isn’t taxable.

- Without a Will: LTT applies if multiple beneficiaries are involved due to consideration for value.

Conclusion

Navigating LTT implications in inheriting Ontario property requires comprehension of tax rules and available exemptions. Seeking professional advice ensures informed decision-making. Understanding LTT nuances aids in managing financial responsibilities effectively during the inheritance process. Consulting experts like real estate lawyers help navigate these complexities, ensuring a smooth property ownership transition.

The intricacies of LTT and its implications for inherited property underscore the need for personalized guidance. While this overview sheds light on general aspects, individual situations may require tailored advice. Understanding LTT intricacies is crucial for managing inheritance-related financial obligations effectively in Ontario.

Be First to Comment